© 2026 «Kompetenz». All rights reserved

Life insurance is one of the most important financial protection instruments for individuals and families. It is designed to provide financial support to beneficiaries if an unexpected loss of life occurs. The policy guarantees that family members or other designated beneficiaries receive a financial payment that helps them maintain economic stability during a difficult and uncertain period.

Unexpected life events may create serious financial challenges for families. A sudden loss of income can affect the ability to pay everyday expenses, maintain housing, continue children's education or meet other long-term financial obligations. Life insurance allows individuals to plan ahead and ensure that their families are financially protected even in situations that cannot be predicted.

The primary purpose of life insurance is to provide financial security to people who depend on the insured individual. By arranging insurance coverage, policyholders create a financial safety mechanism that protects their loved ones against the economic consequences of an unexpected event.

The insurance payment may help families maintain financial stability while adjusting to new circumstances. For many households this financial support becomes essential in covering immediate expenses and preserving long-term financial plans.

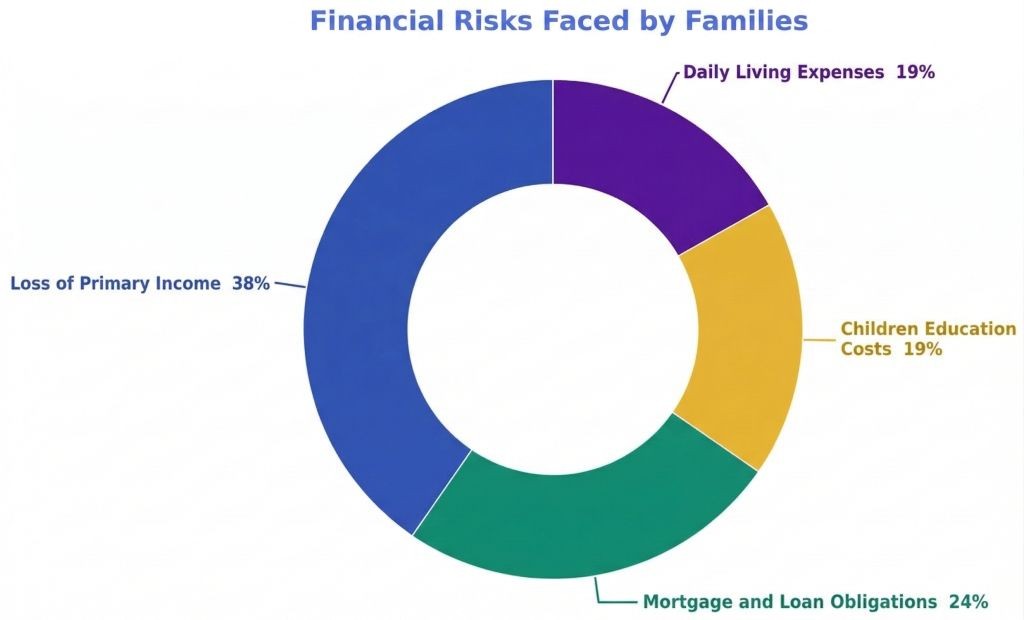

Families often rely on the income of one or more individuals to support their daily lives. If that income suddenly disappears, the financial consequences can be significant. Life insurance helps reduce the impact of several key financial risks.

In many families one or two individuals generate the primary source of income that supports the entire household. If that income is suddenly lost, families may struggle to maintain their normal standard of living. Life insurance provides financial compensation that helps replace lost income and allows family members to adjust to the new financial situation.

Many households have financial commitments such as mortgages, personal loans or credit obligations. Without the income of the insured person, these financial responsibilities may become difficult to manage. Insurance payments may be used to settle outstanding obligations or help families maintain their housing stability.

Parents often plan long-term financial strategies to support their children's education. Unexpected events may disrupt these plans and create uncertainty regarding future educational opportunities. Life insurance payments may provide financial resources to ensure that children can continue their education without interruption.

Regular household expenses such as food, utilities, healthcare and transportation continue even after an unexpected event. Life insurance benefits may help families manage these costs and prevent financial instability during a difficult period of transition.

Life insurance is relevant for a wide range of individuals who have financial responsibilities or dependents. Although the specific needs of each person may vary, insurance protection is commonly considered by people who want to ensure the long-term financial stability of their families.

The insurance payout is provided to beneficiaries specified in the insurance contract. Beneficiaries may use the funds according to their financial needs and priorities.

Typical uses of insurance benefits include:

Life insurance offers several advantages as a financial protection instrument. Its structure is straightforward and focused entirely on providing financial security for beneficiaries.

Responsible financial planning often includes measures designed to protect family members from unexpected events. Life insurance is an effective way to create an additional layer of financial security that helps families maintain stability during uncertain circumstances.

By arranging life insurance coverage, individuals take a proactive step toward protecting their loved ones and ensuring that financial responsibilities can be managed even in challenging situations.