© 2026 «Kompetenz». All rights reserved

Reinsurance is a specialized financial mechanism through which insurance companies transfer part of their risk exposure to other insurers known as reinsurers. This process allows insurers to stabilize financial performance, expand underwriting capacity, and protect their capital from large or catastrophic losses.

Within the global insurance system, reinsurance acts as a structural pillar of risk management. It enables insurers to provide coverage for major industrial projects, large infrastructure developments, multinational corporations, and high-value assets that exceed the capacity of a single insurance company.

Without reinsurance, many sectors of the global economy including energy, aviation, mining, logistics, and technology would face significant barriers in obtaining adequate insurance protection.

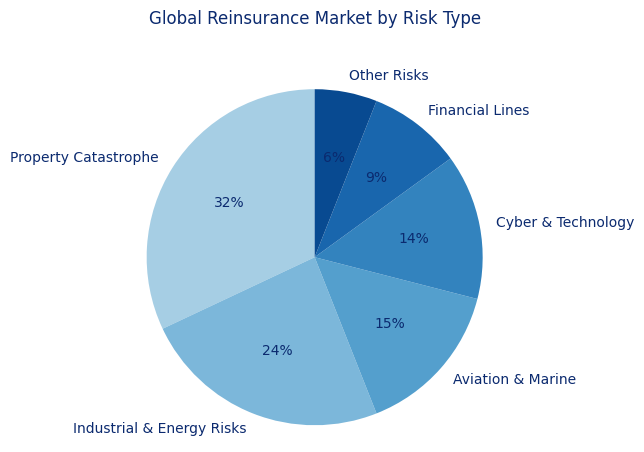

Reinsurance operates as an international risk distribution network. Instead of concentrating financial exposure within a single insurer, risks are distributed across multiple reinsurers located in global insurance hubs such as London, Zurich, Munich, Bermuda, and Singapore.

This structure allows insurance markets to maintain stability even after large catastrophic events such as natural disasters, industrial accidents, or major liability claims.

From a corporate perspective, reinsurance creates "additional insurance capacity" that makes it possible to insure extremely large risks including refineries, airports, manufacturing plants, energy infrastructure, and international transportation networks.

Reinsurance agreements are structured through several models that determine how risk and premiums are shared between insurers and reinsurers.

Facultative Reinsurance

Facultative reinsurance is arranged for a specific individual risk. Each exposure is analyzed separately by the reinsurer. This approach is widely used for complex risks such as industrial plants, energy facilities, aviation fleets, or large construction projects.

Treaty Reinsurance

Treaty reinsurance provides automatic coverage for a defined portfolio of insurance policies. Under this structure, the insurer transfers a predetermined share of risks to reinsurers based on agreed contractual conditions.

Proportional Reinsurance

Under proportional arrangements the reinsurer receives a fixed share of premiums and assumes the same proportion of losses. This method helps insurers expand underwriting capacity while maintaining balanced risk exposure.

Non-Proportional Reinsurance (Excess of Loss)

Non-proportional reinsurance activates when losses exceed a specific threshold. It serves as a "financial shock absorber" protecting insurers from catastrophic claims.

Large corporations frequently require insurance programs with limits far exceeding the capacity of domestic insurance markets. Reinsurance allows insurers to construct multi-layer insurance programs supported by global reinsurance capital.

Such programs typically involve several layers of risk coverage where different reinsurers participate in various parts of the exposure.

Industries most dependent on reinsurance capacity include:

These sectors require "high-capacity insurance programs" often reaching hundreds of millions or even billions of dollars in coverage limits.

Designing and placing reinsurance programs requires access to international markets, deep technical expertise, and advanced risk analytics.

Professional insurance brokers act as strategic intermediaries between insurers, reinsurers, and corporate clients. Their role includes analyzing risk exposure, structuring insurance layers, negotiating with reinsurers, and optimizing coverage terms.

Brokers also coordinate risk engineering surveys, actuarial evaluations, underwriting negotiations, and claims management processes. These steps help reinsurers fully understand the risk profile and ensure fair pricing conditions.

For businesses operating in high-risk industries, reinsurance represents "an invisible financial safety layer" that strengthens the stability of the entire insurance structure.