© 2026 «Kompetenz». All rights reserved

Reinsurance plays a fundamental role in the architecture of the global insurance system. It functions as a financial risk distribution mechanism that enables insurers to transfer portions of their exposure to international reinsurance markets. Through this process the insurance industry can absorb catastrophic losses, maintain solvency, and continue providing coverage for large-scale industrial and infrastructure risks.

This research examines global reinsurance market dynamics, structural trends in risk transfer, the evolution of reinsurance capital, and the growing importance of analytical risk modeling in the placement of large corporate insurance programs.

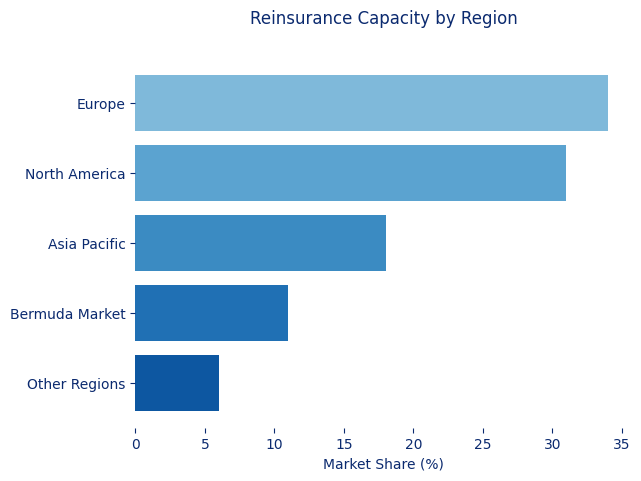

The global reinsurance market represents one of the largest segments of the international financial risk transfer system. According to industry reports published by Swiss Re Institute, Munich Re, and AM Best, total global reinsurance capital exceeded $700 billion in recent years, supported by both traditional reinsurers and alternative capital providers.

The reinsurance market has evolved into a multi-layered financial ecosystem composed of:

This diversification of capital sources has significantly increased the capacity of global reinsurance markets, allowing insurers to underwrite increasingly complex and high-value risks.

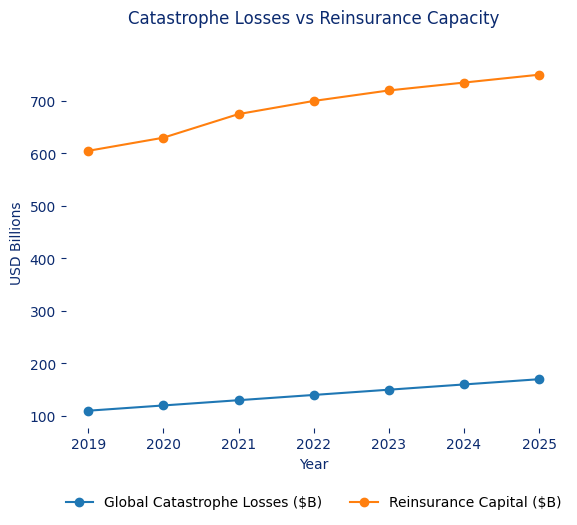

Several structural factors are driving growth in the reinsurance sector. The increasing frequency and severity of catastrophic events has significantly increased the demand for reinsurance protection.

Major demand drivers include:

Natural catastrophes remain the largest source of insured losses worldwide. Hurricanes, earthquakes, floods, and wildfires continue to generate multi-billion dollar claims that require large-scale reinsurance participation.

Large corporate insurance programs typically rely on multi-layer reinsurance structures. These structures distribute risk across several levels of insurance and reinsurance capacity.

The typical structure of a corporate insurance program includes:

This approach ensures that even extremely large industrial losses can be absorbed without threatening the financial stability of a single insurer.

The reinsurance industry is currently undergoing structural transformation driven by technological innovation, advanced analytics, and new capital market instruments.

Several emerging trends are shaping the future of reinsurance:

Catastrophe modeling has become a central component of modern reinsurance underwriting. Advanced models simulate thousands of potential disaster scenarios in order to estimate probable maximum loss levels.

Alternative capital has become one of the most influential developments in the global reinsurance industry. Investment funds, pension funds, and institutional investors increasingly participate in reinsurance markets through structured financial instruments.

Examples include:

These instruments allow investors to participate in insurance risk while providing insurers with additional capital capacity.

Modern reinsurance markets rely heavily on advanced risk modeling techniques. Sophisticated analytics platforms allow insurers and reinsurers to estimate the financial impact of catastrophic events and industrial losses.

Analytical tools commonly used in reinsurance include:

These analytical methods allow reinsurers to price risks accurately and maintain balanced portfolios across geographic regions and industry sectors.

Reinsurance placement is a complex process requiring international market access and technical expertise. Professional insurance brokers play a critical role in structuring reinsurance programs and negotiating terms with global reinsurers.

Brokers typically perform several key functions:

By combining risk analytics with access to global reinsurance markets, brokers help insurers and corporate clients secure large insurance capacities under competitive conditions.

The long-term outlook for the reinsurance sector remains strong. Global economic development, expanding infrastructure investments, and increasing exposure to climate-related risks are expected to drive sustained demand for reinsurance capacity.

At the same time, technological innovation and financial market integration will continue to transform the industry.

The future of reinsurance will increasingly depend on data analytics, global capital flows, and sophisticated risk modeling capabilities that enable insurers to manage complex risk portfolios across industries and geographic regions.