© 2026 «Kompetenz». All rights reserved

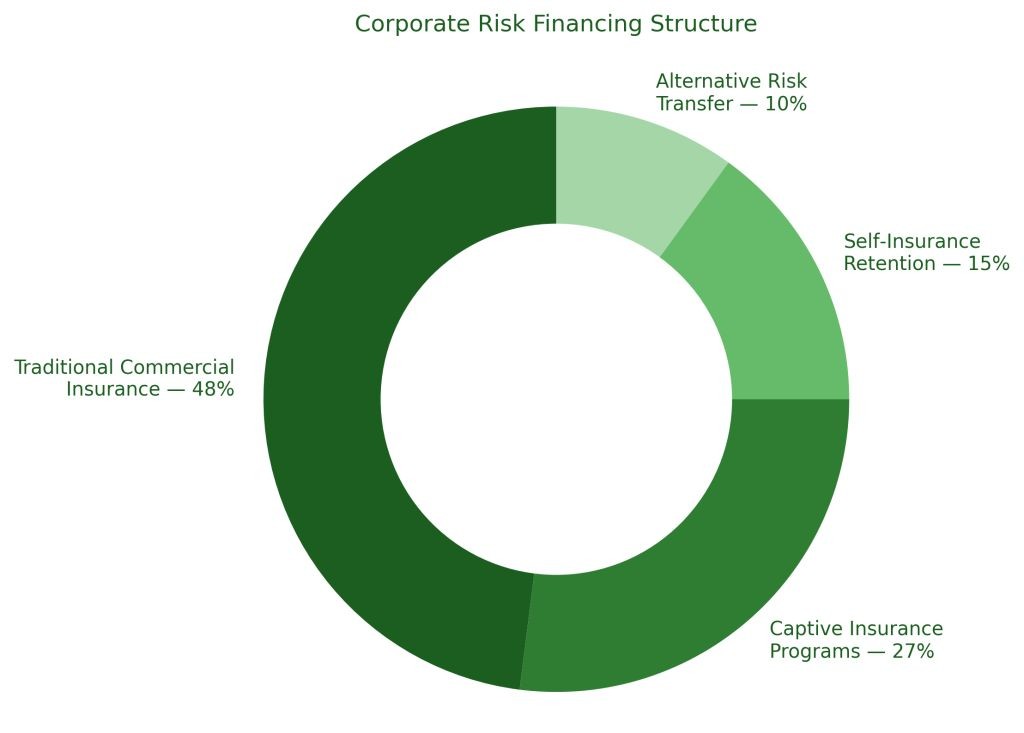

Captive insurance has become an increasingly important risk financing strategy for large corporations and industrial groups seeking greater control over their insurance programs. Instead of relying entirely on traditional commercial insurance markets, companies establish their own insurance entities designed to insure specific risks within the organization.

A captive insurance company is a licensed insurer created and owned by a parent company or group of companies. The purpose of the captive is to provide insurance coverage for the risks of its owners while improving risk management efficiency and optimizing long-term insurance costs.

Captive structures allow organizations to retain predictable risks while transferring catastrophic exposures to the reinsurance market. This approach enables companies to design customized insurance programs that better reflect the operational realities of their business.

The primary objective of captive insurance is to create a more flexible and strategic approach to risk financing. Many large organizations face complex risk exposures that may be difficult or expensive to insure in traditional insurance markets. By forming a captive insurer, companies can retain selected risks internally while purchasing reinsurance for larger exposures.

Captives are commonly used in industries such as energy, manufacturing, mining, transportation and healthcare, where operational risks are highly specialized and insurance costs may fluctuate depending on market conditions.

Captive insurance structures can be organized in several forms depending on the ownership model and the risk profile of participating companies. The most common structure is a single-parent captive, where a corporation establishes an insurance company to insure its own risks.

Group captives are created when several organizations with similar risk exposures form a jointly owned insurance company. These structures allow companies to share risk and benefit from collective purchasing power when accessing reinsurance markets.

Another model includes protected cell captives, which allow different participants to operate separate insurance cells within the same licensed captive structure. This model provides flexibility for organizations that require customized insurance arrangements.

Captive insurance structures provide several strategic advantages in risk management. Organizations gain greater visibility over their loss experience and can implement more targeted loss prevention programs. Because the captive directly insures the parent company’s risks, improvements in operational safety and risk control directly influence the financial performance of the captive.

Captives also allow companies to access global reinsurance markets more efficiently. Instead of purchasing insurance coverage entirely through commercial insurers, the captive can negotiate reinsurance protection for catastrophic exposures.

From a financial perspective, captive insurance structures allow companies to stabilize insurance costs over time. Premiums that would otherwise be paid entirely to commercial insurers can be retained within the captive structure and used to fund future losses or invest in risk prevention programs.

Captives may also improve capital efficiency by allowing organizations to structure insurance programs that reflect the actual risk profile of their operations rather than relying solely on standardized market policies.

For many multinational corporations, captive insurance has become an integral component of enterprise risk management. Captive structures enable companies to integrate insurance, risk management and financial planning into a unified strategy that supports long-term operational stability.

As global business risks continue to evolve, captive insurance solutions are expected to play an increasingly important role in helping organizations manage complex exposures while maintaining greater control over their insurance programs.