© 2026 «Kompetenz». All rights reserved

Captive insurance has become one of the most important instruments of alternative risk financing in the global insurance market. As corporations face increasing operational complexity and volatility in commercial insurance markets, captive insurance structures continue to gain strategic importance. Organizations are increasingly seeking mechanisms that allow greater control over risk financing, premium stability and direct access to global reinsurance markets.

The future development of captive insurance will be influenced by several structural trends shaping corporate risk management and the insurance industry as a whole. These trends include growing demand for alternative risk transfer solutions, expansion of captive domiciles and the increasing integration of captive structures into enterprise risk management frameworks.

Alternative risk transfer mechanisms are expected to play a larger role in corporate insurance programs over the next decade. Many large corporations are moving away from exclusive reliance on traditional commercial insurance markets and are adopting hybrid structures that combine captive insurance, reinsurance and self-insurance retention.

Captive insurers enable organizations to retain predictable operational risks while transferring catastrophic exposures to reinsurance markets. This structure improves financial efficiency and allows companies to design insurance programs tailored to their specific operational risk profile.

Specialized jurisdictions known as captive domiciles continue to expand their regulatory frameworks to attract multinational corporations. Locations such as Bermuda, Cayman Islands, Luxembourg, Guernsey and Singapore remain leading centers for captive insurance operations.

These jurisdictions offer regulatory environments specifically designed for captive insurers while maintaining appropriate solvency oversight. Over the coming years additional regions are expected to develop captive legislation to compete in the global risk financing market.

Captive insurance structures are increasingly integrated into broader enterprise risk management systems. Instead of functioning solely as internal insurance vehicles, captives are evolving into strategic financial instruments that support corporate risk governance and capital planning.

Organizations use captives to collect detailed loss data, analyze operational risk patterns and support long-term financial planning related to risk exposure. This integration improves transparency in corporate risk financing strategies.

New categories of corporate risk are expected to accelerate the development of captive insurance solutions. Cyber risks, climate-related exposures and global supply chain disruptions are increasingly difficult to insure through traditional insurance policies alone.

Captive insurers allow organizations to design specialized coverage structures that address these emerging risk categories while maintaining flexibility in how risk capital is allocated.

The relationship between captive insurers and global reinsurance markets will continue to strengthen. Reinsurers play a crucial role in providing protection against large-scale loss events that exceed the captive’s retention capacity.

Through captive structures, corporations gain more direct access to global reinsurance capacity and can structure layered protection programs that combine internal risk retention with external catastrophic protection.

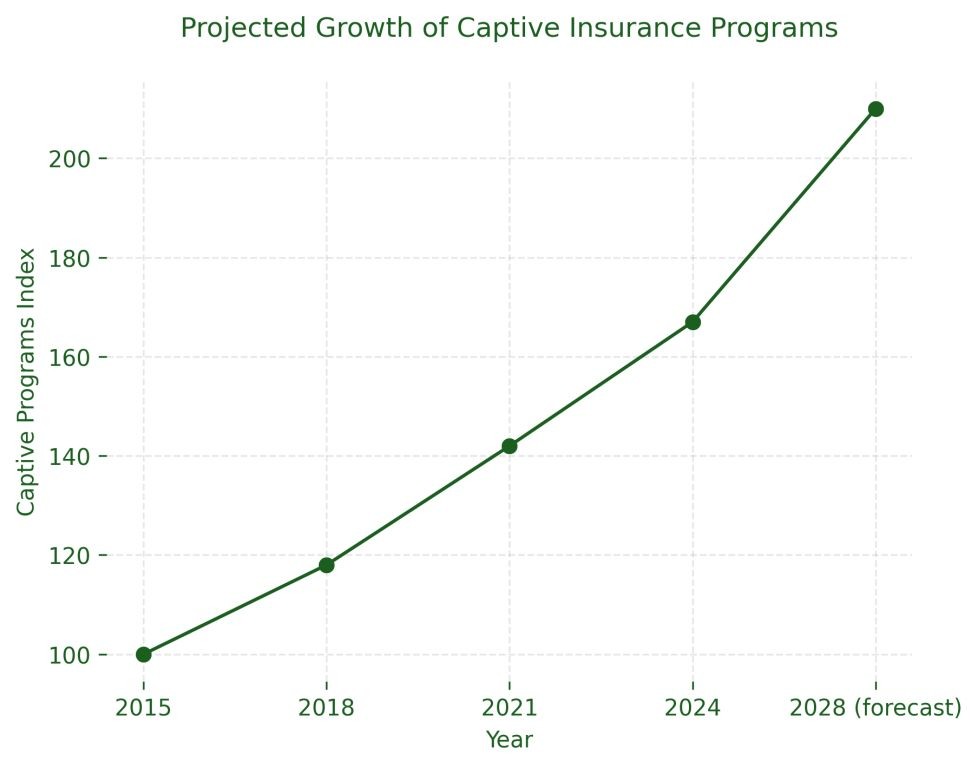

Industry forecasts indicate that captive insurance will remain a core component of advanced corporate risk financing strategies. As companies face increasingly complex operational risks and regulatory environments, captive insurance structures provide flexibility, financial efficiency and improved transparency in managing corporate risk exposure.

Over the next decade, captive insurance programs are expected to expand across multiple industries including energy, healthcare, manufacturing, logistics and technology, reinforcing the role of captives as a strategic instrument in modern risk management.