© 2026 «Kompetenz». All rights reserved

Captive insurance has evolved into one of the most significant components of alternative risk financing for large corporations and multinational groups. A captive insurer is a licensed insurance entity established by a parent organization to insure its own risks. Over the past decades, captive structures have expanded from a niche risk management tool into a widely used mechanism for optimizing insurance programs and improving financial control over corporate risk exposure.

The global captive insurance market continues to grow as companies seek greater flexibility in managing complex operational risks. Industries such as energy, mining, transportation, healthcare, manufacturing and technology increasingly rely on captive insurers to stabilize insurance costs and access reinsurance markets more efficiently.

The number of captive insurance companies worldwide has increased steadily over the last two decades. According to industry estimates, more than 6,000 captive insurers currently operate across major captive domiciles including Bermuda, Cayman Islands, Luxembourg, Guernsey and Singapore.

The expansion of the captive market has been driven by several structural factors. Volatility in traditional insurance markets, particularly during hard market cycles, has encouraged corporations to explore alternative risk financing mechanisms. Captive insurers allow companies to retain predictable risks while transferring catastrophic exposures to the reinsurance market.

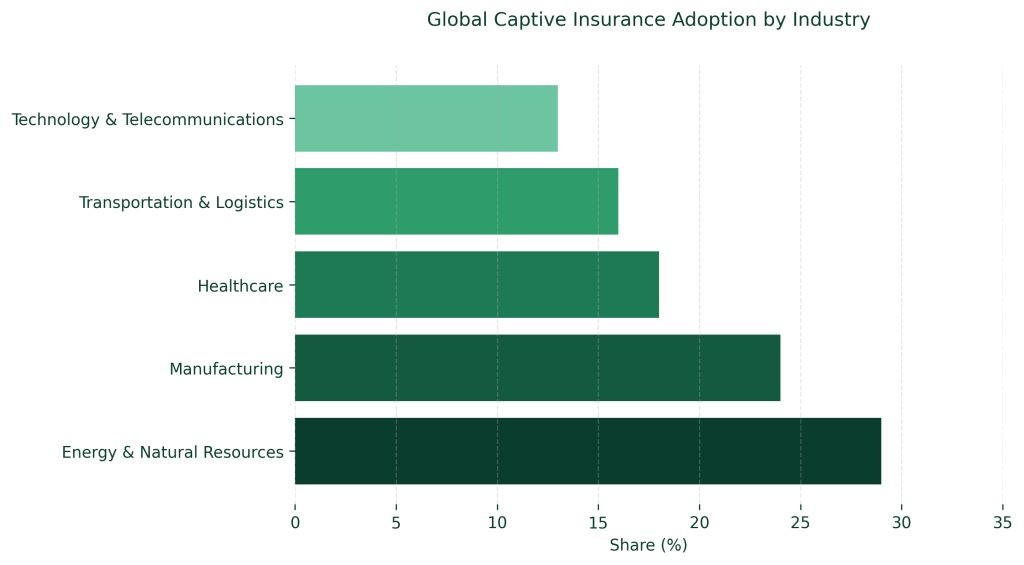

Captive insurance adoption varies across industries depending on risk complexity and capital intensity. Sectors characterized by large operational exposures and significant asset values tend to rely more heavily on captive structures.

Energy and natural resource companies often use captives to insure property risks, environmental liabilities and business interruption exposures. Manufacturing companies frequently establish captives to manage product liability and supply chain risks. Healthcare organizations increasingly use captive insurers to address professional liability and medical malpractice exposure.

Reinsurance plays a critical role in captive insurance programs. While captives retain predictable operational risks, they typically transfer large-scale catastrophic exposures to global reinsurance markets. This structure enables companies to combine internal risk retention with external protection against severe loss events.

Captives also allow organizations to access reinsurance markets more directly. Instead of purchasing insurance solely through commercial insurers, the captive acts as an intermediary risk carrier that structures the insurance program according to the company’s risk profile.

One of the key advantages of captive insurance is improved transparency in risk financing. Because the captive insurer operates within the corporate structure, the parent organization gains detailed insight into its own loss experience and risk drivers.

This visibility enables companies to implement more effective loss prevention strategies and allocate capital more efficiently. Premiums that would otherwise be paid entirely to commercial insurers may be retained within the captive structure and used to fund future losses or support risk mitigation programs.

Captive insurance companies operate within specialized regulatory environments known as captive domiciles. These jurisdictions provide legal frameworks designed specifically for captive insurers while maintaining regulatory oversight and financial solvency standards.

Leading captive domiciles offer regulatory flexibility, tax efficiency and access to global reinsurance markets. As corporate risk management becomes more sophisticated, new jurisdictions continue to develop captive insurance frameworks to attract multinational companies seeking alternative risk financing solutions.

The future development of captive insurance is closely linked to the increasing complexity of corporate risk exposure. Cyber risks, climate-related exposures and global supply chain disruptions are prompting companies to reconsider traditional insurance structures.

Captive insurance structures provide organizations with greater flexibility to adapt to these evolving risks. As global business environments become more uncertain, captives are expected to remain a central component of advanced corporate risk management strategies.