© 2026 «Kompetenz». All rights reserved

The logistics industry is entering a phase of structural transformation where competitive advantage is increasingly defined not only by operational efficiency, but by the ability to manage total risk exposure. Modern supply chains are highly interconnected, creating systemic vulnerabilities where localized disruptions can trigger cascading effects across multiple regions and operations.

In this context, traditional insurance models are no longer sufficient. The market is shifting toward integrated risk management frameworks that combine analytics, insurance structuring, and operational control.

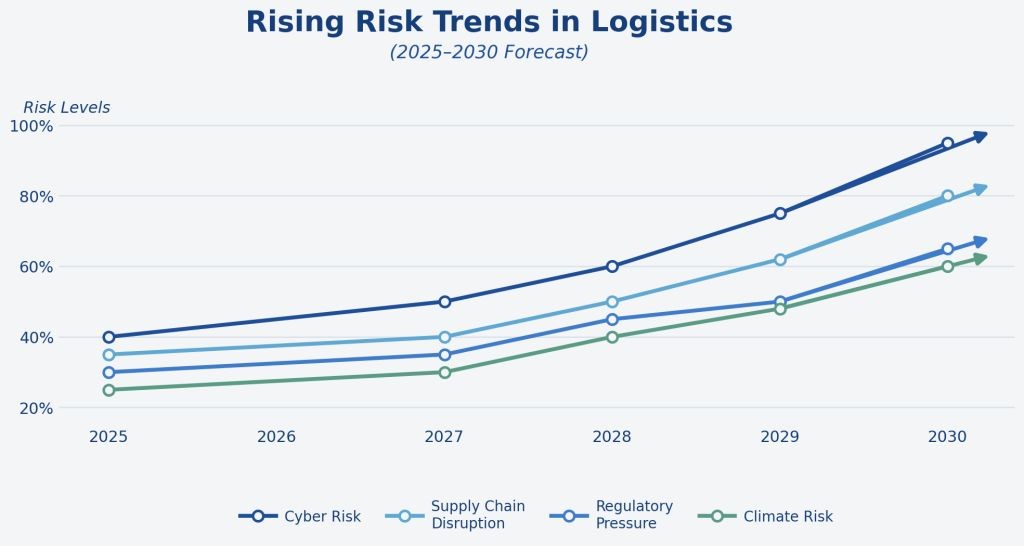

The current risk landscape in logistics is shaped by the simultaneous growth of multiple risk categories, which increasingly reinforce one another.

1. Cyber Risk. The expansion of digital logistics platforms, transportation management systems, warehouse automation, and IoT infrastructure has significantly increased exposure to cyber threats. A single breach can disrupt entire supply chain operations.

2. Supply Chain Disruption. Global trade volatility, geopolitical tensions, and dependency on critical logistics nodes create systemic disruption risks that are difficult to mitigate through traditional contingency planning.

3. Regulatory Pressure. Increasing compliance requirements, customs controls, and ESG-related regulations are introducing new operational constraints, leading to delays, penalties, and higher administrative costs.

4. Climate Risk. Extreme weather events are becoming a structural factor affecting logistics operations, particularly in maritime, rail, and cross-border transportation.

The defining characteristic of this environment is the transition from isolated risk events to interconnected risk systems, where one disruption amplifies multiple downstream impacts.

This shift requires a move from fragmented risk handling toward integrated risk architecture.

The financial dimension of logistics risk is best understood through the Total Cost of Risk framework, which includes insurance premiums, retained losses, and indirect operational impacts.

Organizations adopting structured risk management approaches consistently achieve measurable financial improvements.

1. Reduction of total risk-related costs by approximately 20–35 percent.

2. Decrease in loss frequency by 30–50 percent through preventive measures.

3. Increased predictability of financial outcomes and reduced volatility.

From a strategic perspective, these improvements directly affect EBITDA, capital allocation efficiency, and overall business resilience.

Risk management is therefore evolving into a core financial and strategic function.

Insurance in logistics is transitioning from a reactive loss compensation tool to a proactive risk management instrument.

Key transformation trends include:

1. Integration with operational data. Insurance structures are increasingly based on real-time logistics data, including routes, cargo conditions, and environmental factors.

2. Growth of parametric insurance. Payouts are triggered by predefined events such as delays or disruptions, enabling faster and more transparent claims processes.

3. Consolidation of insurance programs. Companies are integrating cargo, liability, and business interruption coverage into unified frameworks to eliminate inefficiencies and coverage gaps.

4. Customization of insurance solutions. Risk transfer strategies are becoming tailored to specific operational profiles rather than relying on standardized policies.

As a result, insurance becomes a tool for managing the probability and impact of losses rather than merely compensating them.

Technology is a central enabler of advanced risk management in logistics.

1. Predictive analytics. Advanced models allow organizations to anticipate risks and take preventive action before disruptions occur.

2. Digital twins. Virtual representations of supply chains enable simulation of risk scenarios and optimization of operational strategies.

3. IoT-based monitoring. Real-time tracking of cargo conditions reduces damage frequency and enhances transparency for insurers and operators.

4. Blockchain solutions. Distributed ledger technologies support transparency, automate claims processes, and reduce disputes.

Together, these technologies are driving a shift toward proactive and data-driven risk management.

Empirical evidence suggests that many inefficiencies in risk management arise not from lack of data, but from cognitive biases in decision-making.

Organizations tend to underestimate low-frequency, high-impact risks while overestimating more frequent but less severe events. This leads to suboptimal insurance allocation and increased total cost of risk.

Effective risk strategies must therefore incorporate both quantitative analytics and behavioral considerations.

Based on current trends, several structural developments are expected in the logistics sector.

1. Significant growth in cyber-related losses and their share in total claims.

2. Continued increase in insurance costs driven by higher loss severity and frequency.

3. Transition toward dynamic insurance pricing models linked to real-time risk data.

4. Integration of insurance services directly into digital logistics platforms.

Organizations that proactively adapt to these trends will achieve a measurable competitive advantage.

In conclusion, logistics is evolving into a highly data-driven industry where risk management is a central component of strategic governance and long-term value creation.