© 2026 «Kompetenz». All rights reserved

Logistics is often described as a movement function, yet from a risk perspective it is more accurately understood as a system of synchronized dependencies under time pressure. Goods in transit, warehouse inventories, customs processes, transport assets, contractual obligations, digital tracking systems, and third-party service providers form a tightly coupled operational architecture. In such an architecture, risk does not emerge only from isolated damage events. It arises from interruption, accumulation, timing mismatch, liability transfer failures, and the amplification of small operational deviations into material financial loss.

This distinction is critical. Traditional insurance discussions in logistics are frequently organized around product categories such as cargo insurance, motor liability, warehouse protection, or freight forwarder’s liability. That approach is administratively convenient, but analytically incomplete. A serious logistics risk assessment must begin not with insurance products, but with the structure of exposure itself: where value accumulates, where control changes hands, where documentation governs liability, and where delay produces a larger loss than physical damage.

In manufacturing, risk is often concentrated around production assets. In real estate, it is concentrated around physical infrastructure and rental income continuity. In logistics, by contrast, risk is distributed across moving assets, temporary storage points, contractual interfaces, and external networks. This means that the material loss event is only one layer of exposure. The deeper problem lies in the chain reaction triggered by that event.

A damaged cargo unit may generate not only a claim for physical loss, but also missed delivery windows, penalties under service level agreements, spoilage of connected consignments, reputational deterioration with clients, customs complications, and disputes over which party bore the risk at the exact moment of the incident. In other words, logistics losses are frequently multi-vector losses. Their structure is hybrid: part property, part liability, part interruption, part contractual consequence.

This is why insurance design in logistics cannot be reduced to premium comparison. The central professional question is whether the insurance structure reflects the temporal and legal architecture of the logistics chain. If it does not, the insured may discover after a loss that the physical event was covered, but the economically decisive consequence was not.

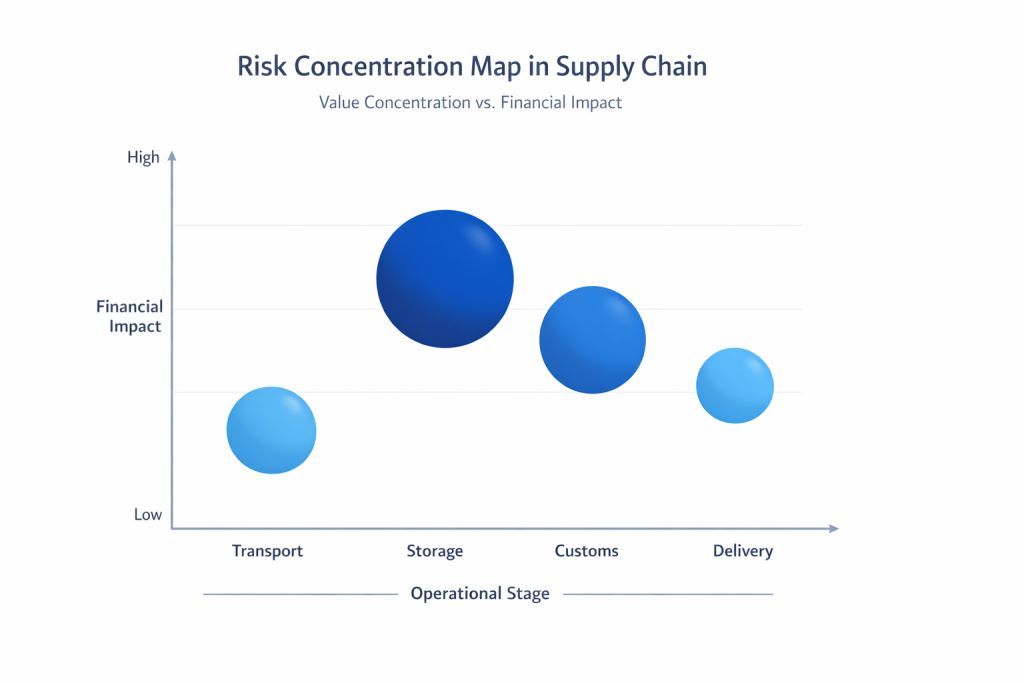

Risk concentration in transit and temporary accumulation points

One of the most underestimated issues in logistics is concentration risk. Many companies perceive logistics exposure as dispersed because cargo is constantly moving. In practice, however, cargo often accumulates at specific nodes: consolidation warehouses, cross-docking points, customs terminals, inland depots, bonded storage facilities, and transshipment locations. These nodes create temporary but significant value concentration.

From an underwriting standpoint, this changes the logic of exposure. The decisive question is not only annual cargo turnover, but peak values at rest, duration of accumulation, storage conditions, fire load, security controls, and the proportion of third-party goods versus owned goods. A logistics operator may believe that its main exposure lies in transit, while its largest uninsured accumulation may in fact sit overnight in a facility treated internally as a routine transfer point rather than a material warehouse risk.

A rigorous reports and research approach therefore examines cargo not merely as moving property, but as a fluctuating pattern of mobile and static exposures. This requires analysis of seasonal peaks, route bottlenecks, transfer delays, storage overflow conditions, and the interaction between declared inventory values and actual high-point accumulation.

The legal fragmentation of liability in logistics chains

Another defining feature of logistics risk is that economic responsibility and legal liability rarely coincide perfectly. Carriers, freight forwarders, warehouse operators, customs brokers, terminal handlers, and subcontracted transport providers may all participate in the same shipment, yet their liabilities arise under different contractual regimes and legal standards. In many cases, liability is limited by convention, contract, or evidentiary threshold rather than by the actual size of the loss.

This creates a recurring strategic misconception. Some businesses assume that because liability exists somewhere in the chain, economic recovery is structurally available. In reality, recovery may be partial, delayed, disputed, or contractually capped. For this reason, a sound logistics risk program must distinguish between three separate categories:

The gap between these three categories is often the real risk. Reports and research work in logistics becomes valuable precisely when it identifies this gap before a dispute occurs. This is especially important in multimodal transport, cross-border trade, and outsourced logistics structures where each segment of the chain may be governed by a different liability logic.

Delay as an independent loss driver

In many sectors served by logistics, time has asset-like value. A missed delivery window in pharmaceuticals, retail distribution, industrial spare parts, or project cargo may generate losses that exceed the cost of physical damage. Yet delay remains one of the least adequately modeled dimensions in many logistics insurance structures.

The reason is conceptual. Physical loss is visible, measurable, and traditionally insurable. Delay is relational. Its financial impact depends on production schedules, sales cycles, contractual commitments, perishability, replacement lead time, and downstream dependency. It therefore requires business-specific modeling rather than generic policy wording.

A mature analytical approach evaluates which cargoes are time-sensitive, which routes are delay-prone, where lead-time compression is impossible, and how quickly service failure propagates through the client’s commercial commitments. This is where practical consulting must go beyond market-standard cargo wording and address the economics of time-critical logistics.

Digital dependence and informational asymmetry

Logistics has become deeply dependent on data integrity. Routing decisions, customs documentation, warehouse management systems, fleet telematics, proof-of-delivery workflows, and client communication are mediated by digital systems. This creates a category of exposure that is neither purely cyber in the traditional sense nor fully operational in the classical sense. It is informational fragility embedded in physical movement.

A digital disruption in logistics does not need to destroy infrastructure to create loss. It may simply corrupt shipment visibility, delay customs filing, interrupt dispatch sequencing, or impair handover verification. The result can be cargo misallocation, detention charges, missed contractual milestones, and disputes over operational responsibility.

From a reports and research perspective, this means logistics analytics must consider informational asymmetry as a risk multiplier. When tracking data, handover documentation, or inventory visibility become unreliable, even a small operational problem becomes harder to attribute, harder to mitigate, and harder to recover financially. This expands both interruption risk and dispute risk.

Insurance implications for logistics operators and cargo interests

A practical implication of this analysis is that logistics insurance should not be constructed as an isolated purchase of separate covers. It should be structured as an exposure map with layered protection. The central task is to determine which risks belong to owned assets, which belong to cargo interests, which belong to legal liability, and which belong to interruption or contract performance.

For cargo owners, the core issue is usually preservation of shipment value, continuity of supply, and reduction of uninsured delay consequences. For logistics operators, the central concern often shifts toward liability assumptions, warehouse accumulation, fleet exposure, subcontractor dependency, and documentation quality. For integrated distribution businesses, both perspectives may coexist, creating hybrid exposure that requires precise segmentation.

In practice, well-designed protection in logistics often depends less on buying more insurance and more on aligning the insurance architecture with operational reality. This includes accurate declaration methods, route-based analysis, warehouse value peaks, contract review, claims protocol design, subcontractor risk standards, and clear allocation of insurable interest.

Claims analysis as a strategic research tool

Claims history in logistics is frequently underused. Many businesses view claims only as a record of past incidents or as evidence for renewal negotiations. In analytical terms, however, claims are one of the most valuable sources of structural intelligence. They reveal where control fails, where packaging is insufficient, where handover procedures are weak, where claims documentation is inadequate, and where contractual assumptions are inconsistent with operational practice.

A sophisticated reports and research approach does not stop at counting claim frequency. It categorizes losses by stage of the chain, by controllability, by documentation quality, by recovery success, by delay consequences, and by recurrence driver. This allows management to distinguish between random volatility and systematic weakness.

That distinction matters commercially. Random volatility may justify risk transfer. Systematic weakness requires operational correction. Without this differentiation, insurance spending often compensates for process defects instead of supporting a resilient logistics model.

Customs, regulation, and border-friction risk

Cross-border logistics adds another layer of complexity: regulatory friction. Customs delays, documentary inconsistency, sanctions-related controls, product classification disputes, and changing import requirements may all create losses that are operationally external but economically direct. Businesses often underestimate these exposures because they are not classical damage events. Yet in international logistics, regulatory interruption can become as costly as physical loss.

This is particularly relevant where cargo is high-value, perishable, compliance-sensitive, or contractually time-bound. The risk is not only seizure or administrative delay itself. It is the resulting cascade: storage extensions, missed delivery obligations, spoilage, contract penalties, and financing pressure.

For this reason, deep logistics analysis must incorporate document governance, jurisdiction-specific compliance risk, and border-process dependency into the exposure model. Any reports and research framework that omits regulatory friction presents an incomplete picture of logistics vulnerability.

What serious logistics research should deliver

A strong logistics reports and research framework should produce more than descriptive commentary. It should identify where exposure accumulates, how value moves, where liability narrows, where delay becomes dominant, and where insurance fails to mirror the real economic structure of the chain. In practical terms, this means the output should help answer a set of business-critical questions:

These questions transform logistics research from a reporting exercise into a management instrument. They allow logistics businesses and cargo owners to reduce volatility, improve contract discipline, optimize insurance structure, and strengthen continuity of supply.

Strategic conclusion

Logistics risk is not defined merely by movement of goods. It is defined by the interaction of time, custody, documentation, concentration, dependency, and legal fragmentation. The deepest exposures often arise not where cargo is most visible, but where responsibility is divided, values accumulate temporarily, or interruption propagates through the chain faster than conventional insurance logic can respond.

A rigorous academic and practical approach to logistics reports and research therefore requires structural analysis rather than generic product description. The objective is to understand how losses are generated, how they compound, and how protection should be aligned with the true mechanics of logistics operations. When that alignment is achieved, insurance stops being a routine procurement line and becomes a disciplined instrument of resilience, continuity, and financial control.