© 2026 «Kompetenz». All rights reserved

The real estate sector is undergoing structural transformation driven by economic volatility, regulatory pressure, technological integration, and changing tenant behavior. These factors are redefining risk exposure and directly influencing how insurance programs should be structured. Industry trend forecasting allows investors, developers, and asset managers to anticipate risks rather than react to them, enabling more resilient and financially efficient decision-making.

Rising interest rates, inflationary construction costs, and capital market tightening are significantly impacting real estate valuations and development feasibility. As financing becomes more expensive, the tolerance for risk decreases, making insurance a critical component of capital protection strategy.

From an insurance perspective, this leads to increased demand for precise asset valuation, stricter underwriting, and a shift toward risk-based pricing models. Properties with higher operational or technical risk profiles face increased premiums and reduced insurer appetite.

The dependency of real estate assets on stable rental income is increasing. Modern commercial properties rely on continuous occupancy, tenant stability, and uninterrupted infrastructure performance. Any disruption, whether caused by physical damage or operational failure, has immediate financial consequences.

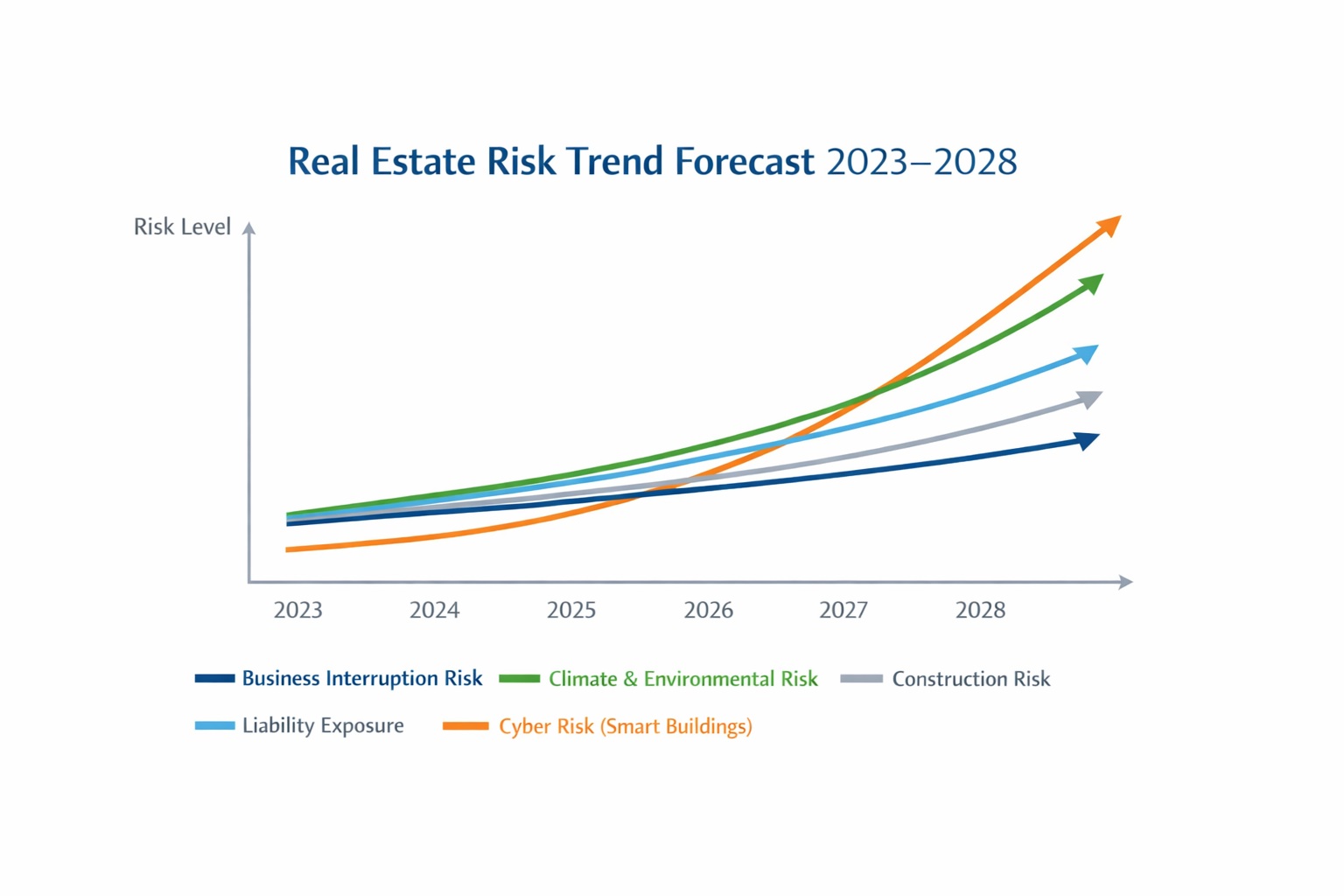

Forecast data indicates a steady increase in claims related to business interruption, particularly in retail, logistics, and mixed-use developments. This trend highlights the need for extended indemnity periods and more accurate income modeling in insurance programs.

Development projects are becoming more complex due to advanced engineering solutions, sustainability requirements, and tighter project timelines. This increases exposure to design errors, contractor coordination failures, and supply chain disruptions.

Forecast trends show higher frequency of losses during construction phases, especially in large-scale urban developments. As a result, insurers are placing greater emphasis on engineering surveys, project risk assessments, and detailed underwriting information before offering coverage.

Environmental factors are becoming one of the most critical drivers of real estate risk. Flooding, extreme weather events, and temperature-related stress on infrastructure are increasing both the frequency and severity of property damage claims.

Real estate portfolios located in high-risk zones face growing insurance costs and, in some cases, limited availability of coverage. This trend is expected to intensify, requiring proactive mitigation measures such as infrastructure upgrades, site-specific risk engineering, and adaptive insurance structuring.

The integration of digital systems into real estate operations introduces new categories of risk. Smart buildings, automated systems, IoT infrastructure, and centralized management platforms improve efficiency but increase exposure to cyber threats and system failures.

Forecasts indicate a steady rise in cyber-related incidents affecting property management systems, access control, and operational continuity. This requires the integration of cyber insurance into traditional property programs.

Increasing regulatory requirements and higher expectations for safety and compliance are expanding liability exposure for property owners and developers. This includes tenant safety, public access areas, environmental compliance, and contractor responsibility.

Forecast trends show a gradual increase in liability claims, particularly in high-traffic commercial properties. Insurance structures must evolve to include broader liability protection and higher coverage limits.

The traditional approach of treating insurance as a standalone function is becoming obsolete. Real estate stakeholders are increasingly adopting integrated risk management frameworks that combine insurance, risk engineering, operational controls, and financial planning.

This shift allows for better alignment between insurance coverage and actual exposure, improving both cost efficiency and protection quality. It also supports more informed decision-making at the investment and portfolio management level.

Over the next 3–5 years, the real estate insurance landscape is expected to be shaped by higher risk sensitivity, more selective underwriting, and increased demand for data-driven insurance solutions. Asset owners who proactively adapt to these trends will achieve stronger financial resilience and better long-term performance.

The ability to anticipate risk, rather than respond to it, will define competitive advantage in the evolving real estate market.