© 2026 «Kompetenz». All rights reserved

Real estate assets require structured insurance solutions that go beyond standard coverage. Practical implementation of risk management strategies demonstrates measurable financial impact, including cost optimization, improved protection levels, and enhanced investment stability. Below are selected real estate cases illustrating how tailored insurance programs deliver tangible business results.

A multi-building office portfolio with a total area exceeding 25,000 sqm operated under fragmented insurance policies issued by different insurers over several years. The structure led to duplicated coverage, inconsistent limits, and lack of business interruption protection.

A full risk assessment was conducted, including property valuation review, exposure mapping, and claims history analysis. The insurance program was consolidated into a single structured placement, incorporating property damage, machinery breakdown, and business interruption aligned with rental income flows.

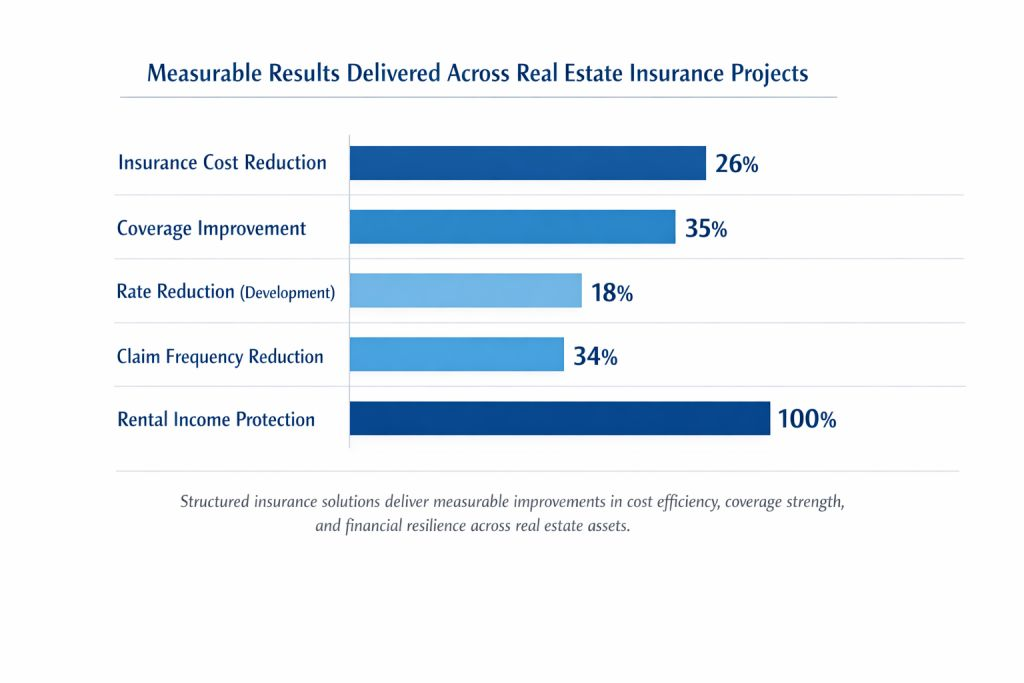

As a result, total insurance costs were reduced by 26%, while coverage limits increased by more than 35%. The updated program also improved claims handling speed and reduced administrative complexity across assets.

Centralized structuring enabled better control over risk financing and improved overall portfolio efficiency.

A large-scale residential construction project faced significant exposure to construction risks, contractor liabilities, and lender-driven insurance requirements. The project lacked a comprehensive insurance framework aligned with international standards.

A Construction All Risks (CAR) program was designed, supported by engineering risk analysis and detailed underwriting preparation. The placement included third-party liability coverage and was structured with access to international reinsurance capacity.

The project secured financing without delays, achieved an 18% reduction in insurance rates, and ensured full compliance with bank requirements. The insurance structure also reduced the probability of project interruption due to unforeseen events.

Insurance became a facilitating tool for capital привлечения and project continuity.

A logistics operator managing multiple warehouse facilities experienced recurring losses related to fire exposure, equipment damage, and operational disruptions. Insurance policies were inconsistent across locations and did not reflect real operational risks.

A unified insurance program was implemented, including property damage, liability coverage, and business interruption. In parallel, risk engineering measures were introduced, including fire system upgrades and improved security protocols.

The result was a 34% reduction in claim frequency and improved underwriting terms, including lower deductibles and broader coverage conditions. Operational continuity improved significantly, reducing financial volatility.

Integration of insurance and risk engineering produced a measurable reduction in loss exposure.

A private investor managing premium residential properties faced underinsurance risks due to outdated asset valuations and absence of liability coverage related to tenants and third parties.

The solution included full asset revaluation, implementation of a portfolio-level insurance structure, and inclusion of landlord liability coverage. Policy conditions were aligned with actual market value and tenant exposure.

The updated program ensured full asset protection, reduced exposure to third-party claims, and optimized the premium-to-coverage ratio across the portfolio.

Portfolio-based structuring proved more effective than fragmented policy placement.

A retail property with high tenant turnover and dependency on anchor tenants faced significant exposure to loss of rental income in case of operational disruption. Existing insurance coverage focused only on physical damage.

A business interruption model was developed based on rental flow analysis, tenant dependency structure, and expected restoration timelines. The insurance program was updated to include extended indemnity periods and coverage for loss of rent.

As a result, the property achieved full protection against income disruption scenarios, improving financial predictability and investor confidence.

Income protection became a key component of overall asset resilience.

Across all cases, the implementation of structured insurance solutions resulted in measurable improvements in cost efficiency, coverage adequacy, and operational stability. Real estate insurance, when designed correctly, functions not as an expense but as a strategic financial instrument that protects income, supports financing, and enhances asset value.